Who is Actually Winning the Content Game

FSW unveils the inaugural cross-sectoral IWT Content Effectiveness Index and what it reveals about competitive advantage in the AI era.

“A system is perfectly designed to get the results it gets.”

— W. Edwards Deming

Insights

Differentiation is now structural, not creative. Performance gaps are widening across industries because some organisations operate with coherent content systems while others do not. Creative output and AI adoption alone no longer explain growth or stagnation.

Content architecture has become a growth variable. Organisations with defined narrative systems, clear audience logic, and operationalised content governance consistently outperform peers across revenue growth, trust, and strategic agility.

AI amplifies existing content maturity. AI rewards coherence and penalises fragmentation. Where content systems are strong, AI quietly increases scale and efficiency. Where systems are weak, AI increases noise, risk, and sameness.

“Content hysteresis” is suppressing performance. Years of campaign-led and trend-reactive content decisions have embedded narrative debt into many organisations. This debt slows differentiation and makes strategic change difficult even when leadership and strategy evolve.

Fewer, clearer stories now outperform volume. In an information-saturated media landscape, clarity, consistency, and narrative restraint have become signals of institutional strength. The most effective organisations communicate less, but with greater coherence and durability.

Introduction: Differentiation in the Age of AI

This is the first cross-sectoral content strategy and competitiveness report produced by the research team at It’s A Working Title LLC (IWT). Prior reports have drilled deeply into sector-specific content assessments and ranked individual firms, and even brands, to understand the drivers of competitive differentiation and growth. In this study, we examine content quality and the factors that drive it across 13 sectoral verticals.

Across industries, organisations are investing heavily in AI to transform how they communicate, market, scale, and do business. Yet, in spite of near-universal access to the same tools, performance outcomes are diverging rather than converging. Some organisations are pulling away from peers operating under identical economic and technological conditions. Others are producing more content than ever with diminishing returns.

With lessons learned from our work on systems content strategy and AI with a range of clients, this report finds that cross-firm distinctions in content effectiveness are not organisational or creative capability, platform strategy, or even AI sophistication. They are the result of investment in content strategy systems.

In this report, we argue that we are entering a differentiation economy in which growth accrues to organisations with coherent content systems and defined narrative architectures. In this environment, content is no longer a downstream expression or result of strategy. Content is, in fact, a governing system that shapes how strategy is understood, trusted, interpreted, and sustained over time.

Our cross-sectoral analysis shows a clear relationship between content effectiveness and performance. Organisations that treat content as an extension of corporate strategy and as essential operational infrastructure rather than marketing output are better positioned to:

Communicate consistently across moments of change

Build trust with increasingly fragmented audiences

Flex with new technologies without destabilising their brand

Scale meaning without increasing noise

By contrast, organisations operating with fragmented, campaign-led content ecosystems are experiencing what we describe as content hysteresis. Past content decisions continue to shape perception, workflows, and audience trust long after those tactics have stopped working. Narrative debt accumulates quietly, limiting differentiation and slowing strategic repositioning.

Unfortunately, in these circumstances, using AI does not resolve these internal organisational tensions. It exposes it.

Where content systems are coherent, AI functions as quiet infrastructure. It improves consistency, streamlines processes, accelerates reuse, and reduces operational friction. Where content systems are fragmented, AI increases volume without clarity and amplifies sameness. The technology itself is not the differentiator. The system into which it enters is.

This inaugural cross-sectoral IWT Content Effectiveness Index examines why some sectors have structurally outperformed others in the AI era. The patterns identified here now apply across enterprise technology, financial services, infrastructure, consumer sectors, healthcare, and media, among other sectors.

The central question is no longer whether organisations should adopt AI for content. The question is whether their content ecosystems are structurally ready or capable of supporting differentiation at scale.

The sections that follow examine how content systems, narrative coherence, and the right operational infrastructure for content determine which organisations grow, which stagnate, and which struggle to be understood at all.

AI does not create differentiation.

It reveals which organisations have structured, intentional content systems and which do not.

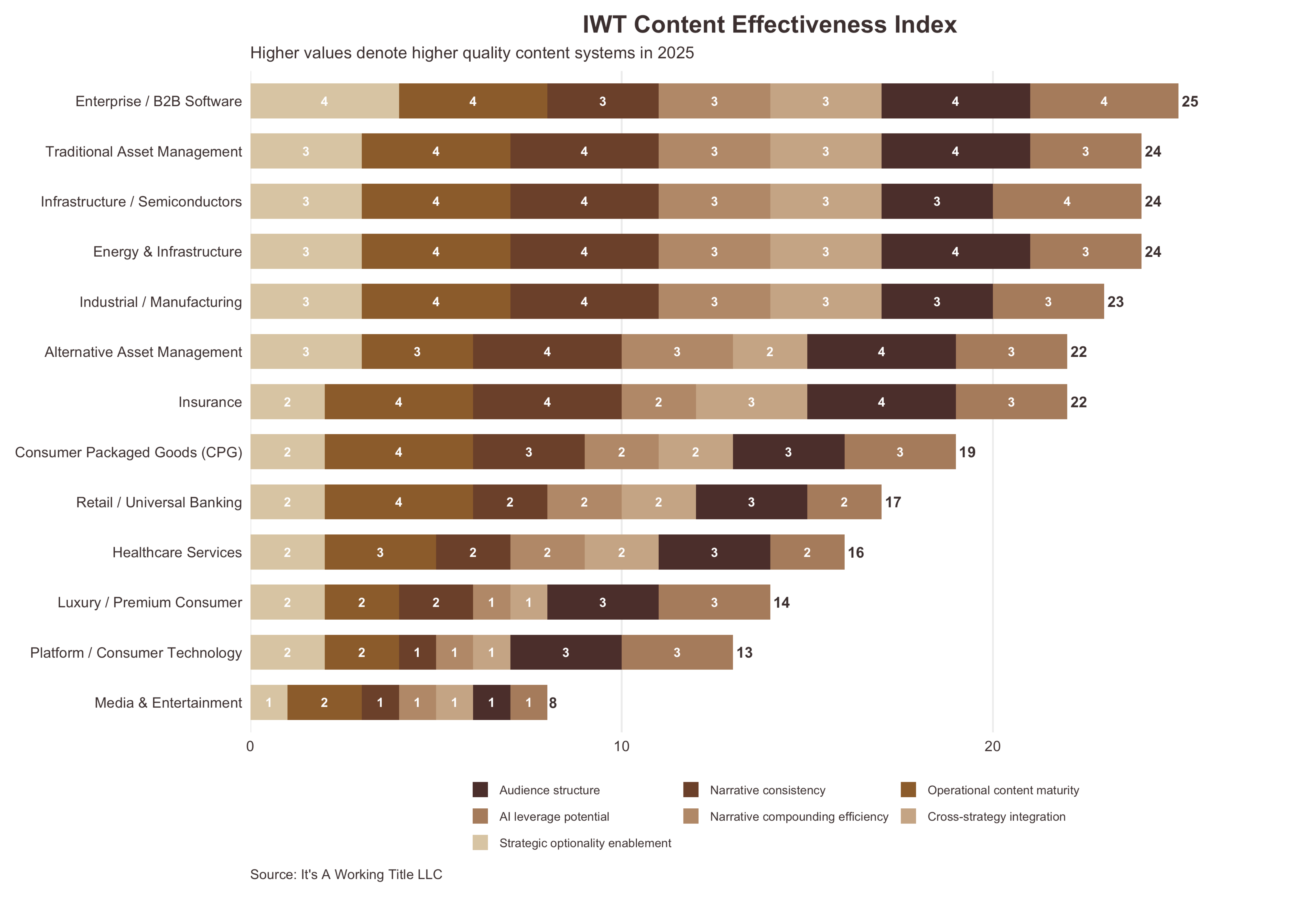

The Content Effectiveness Gap Across Industries

Before looking at sector-level performance, it is worth clarifying what sets apart high-performing organisations from the rest in the current environment. The differences are not a matter of creativity, channel mix, technology adoption, or even content quality. They are the result of structural investment in content strategy systems: the narrative frameworks, governance models, operating processes, and decision rules that determine what content is created, how it is expressed, and how it scales over time.

Across industries in our client work, we see the same pattern over and over again. Organisations that operate with coherent narrative systems and defined content operations are able to communicate consistently, scale meaningfully, and absorb new tools without destabilising their identity. Those that do not struggle to convert activity into advantage, even as investment increases, producing content is tactical rather than strategic, optimized for short-term impact but poorly aligned with corporate objectives or the changing needs, contexts, and expectations of target audiences.

The analysis that follows examines how these organisational differences in content effectiveness show up at the sector level. Rather than focusing on individual brands or platforms, we examine how entire industries tend to organise, think about, and create content, and why those choices are increasingly predictive of performance in the AI era.

At a high level, sectors cluster into three broad groups. While individual organisations can and do outperform their peers, these clusters reflect common structural tendencies rather than isolated success or failure.

Sectors at the top of the IWT Content Effectiveness Index include: enterprise and B2B software, infrastructure and semiconductors, energy and industrial systems, and asset and wealth management. These industries operate in complex, high-stakes environments where clarity, consistency, and trust are non-negotiable. As a result, content is often treated as a core strategic asset rather than a marketing output.

In these top-performing sectors, content systems are frequently characterised by:

Clear narrative hierarchies that connect strategy to execution

Defined audience segmentation across customers, partners, regulators, and investors

Defined content governance around language, policies, and tone

Content designed for reuse, longevity, and consistency across channels

These structural choices make it easier for organisations to scale communication without losing meaning. They also create conditions into which AI can be introduced as infrastructure, supporting modularisation, formatting, and distribution without destabilising narrative coherence.

By contrast, mid-performing sectors display partial or incomplete content maturity. They may have well-articulated brand narratives but struggle to express them consistently across touchpoints. Content may be strong in flagship moments or channels, but weaker elsewhere. Operational inconsistency, rather than a lack of vision, is often the limiting factor.

Common characteristics of this mid-performing group include:

Strong top-line storytelling but uneven execution

Inconsistent audience logic across channels

Campaign-led planning that impedes narrative continuity

Limited content reuse across formats and markets

At the lower end of the index sit sectors such as media and entertainment, platform-driven consumer technology, and parts of consumer lifestyle and luxury. In spite of being highly creative and content-intensive, these industries tend to suffer from fragmentation and information dilution. Content production is often driven by platform incentives, trend cycles, and short-term performance metrics rather than long-term narrative coherence.

In these environments, organisations in the lower-performing group often face:

High content volume with low narrative memory

Frequent shifts in tone, message, and positioning

Overreliance on novelty, virality, and reactive formats

Limited structural distinction between competitors

Over time, these patterns produce what appears to be differentiation on the surface but, in fact, is sameness in practice. As content accelerates, meaning erodes and brand identity for these organisations can become less potent and distinct.

What this cross-sectoral IWT Content Effectiveness Index ultimately shows is not a hierarchy of creativity or innovation. But rather, it reveals a hierarchy of content discipline. Some sectors have been forced by regulation, complexity, or risk to build content systems that prioritise clarity and coherence. Others, despite greater creative freedom, have allowed fragmentation to accumulate unchecked.

As the next section explores, these differences become far more consequential in an AI-mediated environment. AI does not smooth over structural weaknesses. It amplifies them. The sectors that have invested in content discipline are positioned to benefit quietly and compounding. Those that have not are likely to find that increased speed and volume only deepen existing challenges.

Content Hysteresis and the AI Amplification Effect

The performance gaps described in the previous section are not solely the result of present-day organisational choices. They are the cumulative outcome of how organisations have structured, governed, and resourced content over time. As AI adoption accelerates, these long-standing decisions are no longer latent. They are being surfaced, stressed, and, in many cases, exposed. This section examines the concept of content hysteresis to explain why some organisations adapt smoothly to change while others struggle and how AI acts as an amplifier of these underlying structural conditions.

As organisations accelerate AI adoption, many are discovering that transformation is not frictionless. This is due to content hysteresis: the lingering impact of “narrative debt” or past organisational approaches to content creation, management, and governance—both internally across teams and workflows and externally across channels, touchpoints, and audiences—on present and future performance.

Content hysteresis occurs when fragmented narratives, inconsistent messaging, and siloed workflows continue to shape perception and operations long after the tactics that produced them have stopped working. These patterns persist across internal processes and external communications alike. Change is not immediate or reversible. Organisations cannot simply decide to become coherent or differentiated. Narrative debt must be actively unwound. AI intensifies this dynamic by accelerating the reproduction of existing structures, whether sound or flawed.

Where content systems are coherent, AI functions as a stabiliser. It supports consistency, accelerates reuse, and reduces operational friction.

Where content systems are fragmented, AI accelerates failure. It increases volume without clarity, accelerates inconsistency, and amplifies sameness.

This explains why AI investment outcomes vary so widely across sectors. The technology itself is not the differentiator. The system to which it is applied is.

In our work, we consistently observe the following patterns:

Organisations using AI primarily to generate content struggle with trust and differentiation

Organisations using AI to govern, structure, and adapt content gain scale without dilution

Higher visibility of AI correlates with weaker narrative outcomes

Structural coherence is the primary determinant of return on AI investment

AI does not fix an organisation’s content problems. It makes them impossible to ignore.

The Differentiation Economy: Why Fewer, Cleaner Stories Win

The patterns outlined in this report point to a fundamental shift in how advantage is created and sustained. As AI accelerates production, distribution, and optimisation, differentiation is no longer determined by who can say the most, the fastest, or with the greatest technological sophistication. It is determined by whether an organisation has built the structural conditions required for its story to remain intelligible, credible, and coherent as it scales.

We are now operating in a differentiation economy. Growth no longer accrues evenly across categories. It accrues to organisations with structural narrative advantage: those that have invested in content systems capable of carrying meaning consistently across teams, channels, and time.

In this environment, many long-held assumptions about content and communication no longer hold:

Volume is not relevance

Speed is not intelligence

Technology is not trust

What matters instead is whether an organisation can be consistently understood by customers, partners, employees, and markets across moments of growth, pressure, and change. Narrative legibility and distinction, if you will, have become a competitive asset.

High-performing organisations communicate less, but with greater clarity. They produce fewer content types with stronger connective tissue.

High-performing organisations communicate less, but with greater clarity. They produce fewer content types with stronger connective tissue between strategy, execution, and experience. Rather than constantly reinventing themselves through campaigns, they invest in recognisable narrative worlds that audiences learn to understand, trust, believe in, and return to. Simplicity becomes a signal of confidence, not constraint.

This shift does not diminish creativity. It protects it. Structure and systemisation allow creativity to compound. When teams are no longer renegotiating tone, message, or format with every content initiative, they can focus on deeper storytelling, richer experiences, and more meaningful innovation. Coherence reduces friction; and reduced friction creates space for better work.

The organisations that define the next phase of growth in an AI-mediated economy will not be the loudest or the most technologically visible. They will be the ones with clear boundaries, consistent narratives, and content systems strong enough to hold meaning as they scale. They will feel different because their choices are deliberate—and because those choices endure.

AI has not changed what actually creates differentiation. It has removed the ability to hide. Organisations can no longer rely on novelty, volume, or tools to substitute for clarity. Meaning must be designed, governed, and maintained, or it will disappear under scale.