Luxury Strategy Planning Under Persistent Inflation Uncertainty (web version)

A new It's A Working Title white paper argues that a scenario-based approach to strategy is essential for the luxury industry in a turbulent market environment

Summary

The level of inflation matters less for luxury planning than its volatility. Economies and firms can adapt to inflation that is high or low, provided it is stable, because stable conditions can be priced into plans. What they struggle to absorb is inflation that moves. The past eighteen months have given luxury a concentrated version of this problem: gold rose by more than half over 2025 and peaked above five thousand four hundred dollars an ounce in January 2026, US tariffs reset landed costs mid-cycle, and wages, logistics and financing costs shifted at different speeds across markets. No single pressure would have overwhelmed the industry. Their combination, and the speed at which each can change, has made planning assumptions expire faster than the plans built on them.

Luxury is more exposed to this dynamic than most consumer industries. In luxury, price is not simply a commercial variable; it is part of the product, communicating scarcity, craft and position, and it moves in practice in only one direction. A consumer goods company facing volatile costs can raise prices, lower them and discount as conditions change. A luxury house cannot do this without eroding the desirability that justifies the price, so an increase, once taken, is difficult to reverse. Nor do the inputs offer relief: gold cannot be substituted, artisan labour cannot be scaled on demand, and heritage production cannot be relocated to follow a tariff. The industry is absorbing volatile costs through one of the least flexible pricing models in the consumer economy.

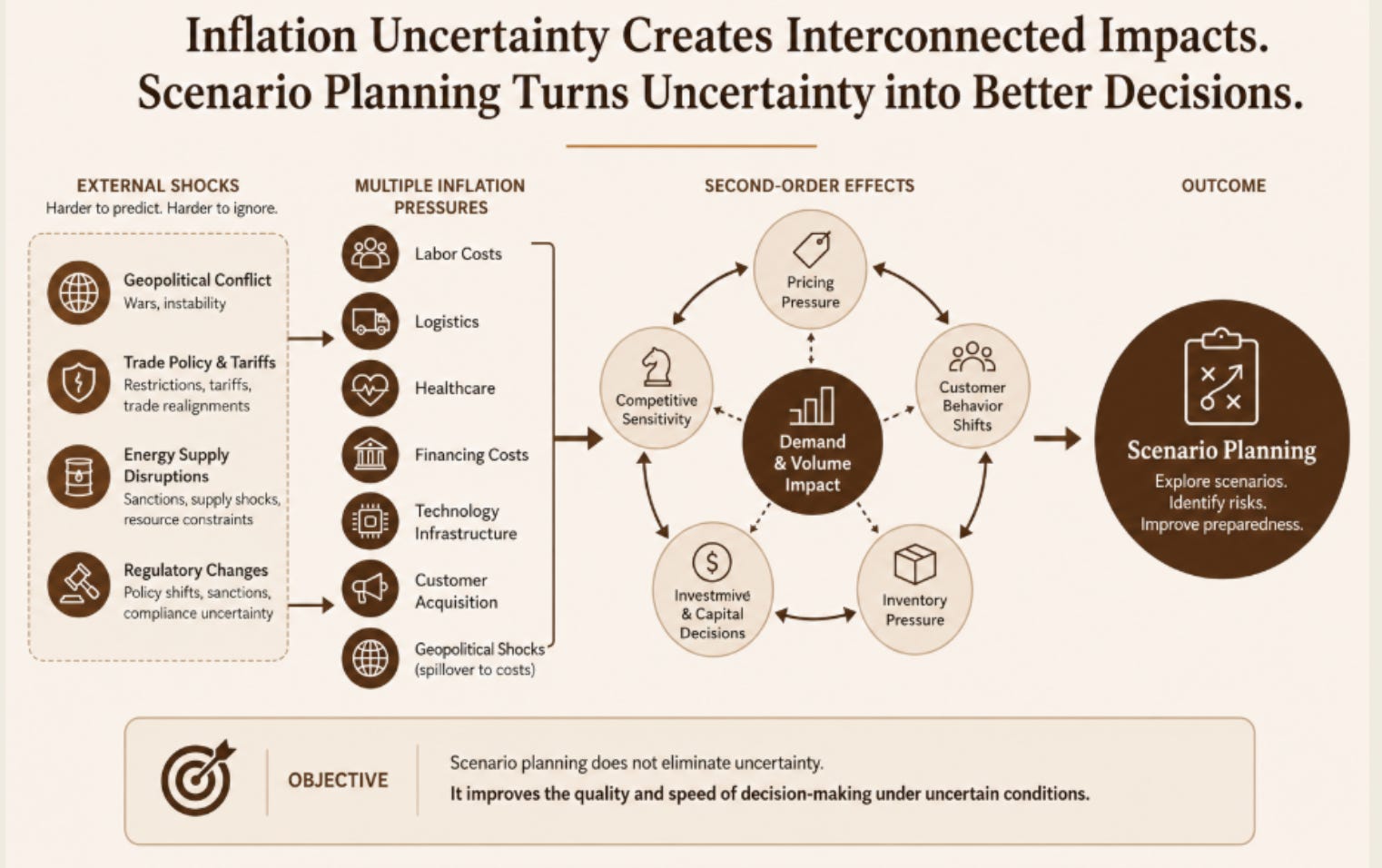

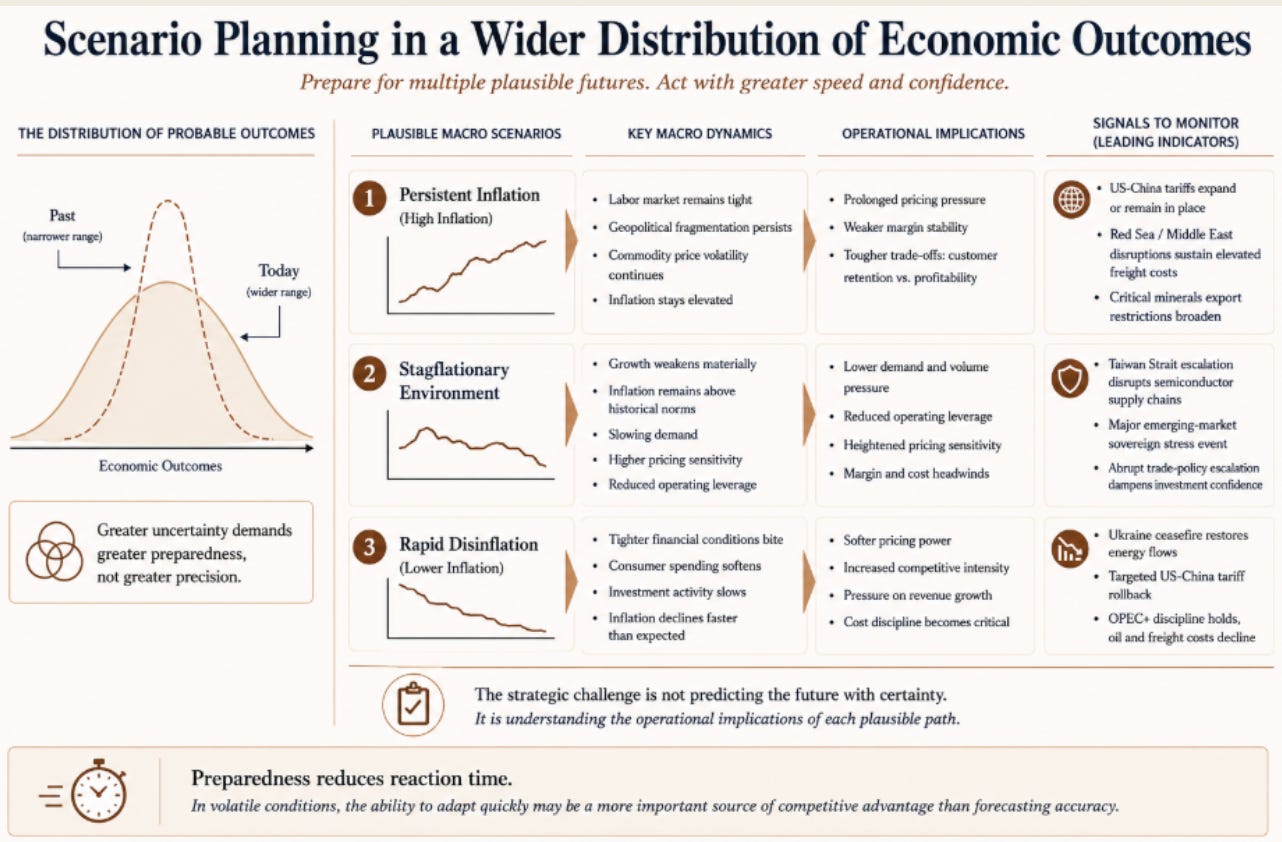

This is why we believe scenario planning, rather than improved forecasting, is the more useful response. The objective is not to predict where inflation settles, but to understand the operational implications of several plausible paths before any of them arrives. This paper examines three: persistent cost pressure, a stagflationary combination of soft demand and sticky costs, and a rapid disinflation in which elevated price structures may need to be unwound. Each carries different implications for pricing governance, sourcing, allocation and client strategy, and each can be distinguished in advance through specific signals, from precious-material prices and US tariffs to Swiss export data, Chinese confidence and the secondary market.

The broader message for enterprise luxury businesses is preparedness rather than prediction. Houses that have rehearsed alternative conditions respond faster and with more conviction when conditions change, and in a category where a mistimed pricing decision costs both margin and desirability, reaction time has become a genuine source of advantage.

The End of the Pricing-Power Assumption in Luxury

For much of the past decade, most luxury houses approached pricing as a lever that could be pulled almost indefinitely. The logic was coherent on its own terms. Scarcity sustained desirability, desirability sustained pricing power, and pricing power funded the scarcity that began the loop. Raising prices was not merely defensible; it was strategic. The demand surge that followed the pandemic, with entry prices on flagship handbags rising by half or more in a few seasons, appeared to confirm it.

That loop rested on conditions now shifting at once. The globalization regime that shaped the wider economy was disinflationary, and luxury benefited twice over: as a buyer of inputs through stable, integrated supply chains, and as a seller to a client base that expanded year after year. Costs were contained. The aspirational middle grew. The top of the market deepened. Houses optimized around price, exclusivity and margin precisely because the environment rewarded those choices. Today several of those conditions are under pressure simultaneously, from input costs to trade policy to the patience of the client.

Gold and skilled labor have made input costs volatile rather than benign. Trade fragmentation has turned the route to market into a cost and a question. The aspirational client, long treated as inexhaustible, has thinned, priced out by the elevation that drove recent growth and, in the Bain reading, resentful of increases that arrived without matching creativity. A structural shift from owning objects toward experiences is redirecting spending away from goods.

It suggests something more consequential for planning: that the unusually favorable conditions of the last cycle, in which price could be raised almost without consequence, may not return in the same form on the forecastable horizon. For leadership teams, the distinction matters.

Traditional luxury planning was built around a narrow band of expected outcomes, in which most pressures could be absorbed through a further increase in price. The band has widened. Pricing dynamics, input costs, trade conditions and client sentiment can now move further and faster than most operating models were built to manage. Deviations once absorbed through routine adjustment now compound across margin, volume and brand perception at the same time.

Volatility itself has become a core strategic variable for luxury.

Inflation as a Multi-Dimensional Strategic Force

Inflation reaches luxury houses through several channels at once, and the interactions between them are where the difficulty lies. Pricing pressure is no longer confined to a single input. It is layered across raw materials, skilled labor, logistics, trade duties, financing and the cost of acquiring and retaining clients. This complexity produces second-order effects that conventional planning, calibrated on a more stable era, tends to underestimate.

Consider the most immediate channel, input costs. Gold rose more than half over 2025 and peaked above five thousand four hundred dollars an ounce in January 2026, with the quarterly average itself a record. When an input moves that far within weeks, a jewelry house priced on a quarterly cadence finds its margins eroded before the next review. When a tariff resets the landed cost mid-cycle, the pricing decision cannot wait for the annual plan. And when price is raised to recover an input or a duty, the increase does not stop at the margin line: it alters client behavior, sharpens scrutiny of value, and feeds back into volume and allocation.

The point is not that forecasting loses value. It is that its role changes. Under stable conditions, forecasting served to optimize around a predictable base. Under structural uncertainty it becomes a means of rehearsing alternative futures, identifying the signals that distinguish them, and shortening the time between a change in conditions and a decision.

The objective of scenario planning is not to eliminate uncertainty. It is to improve the quality and speed of the decisions taken within it.

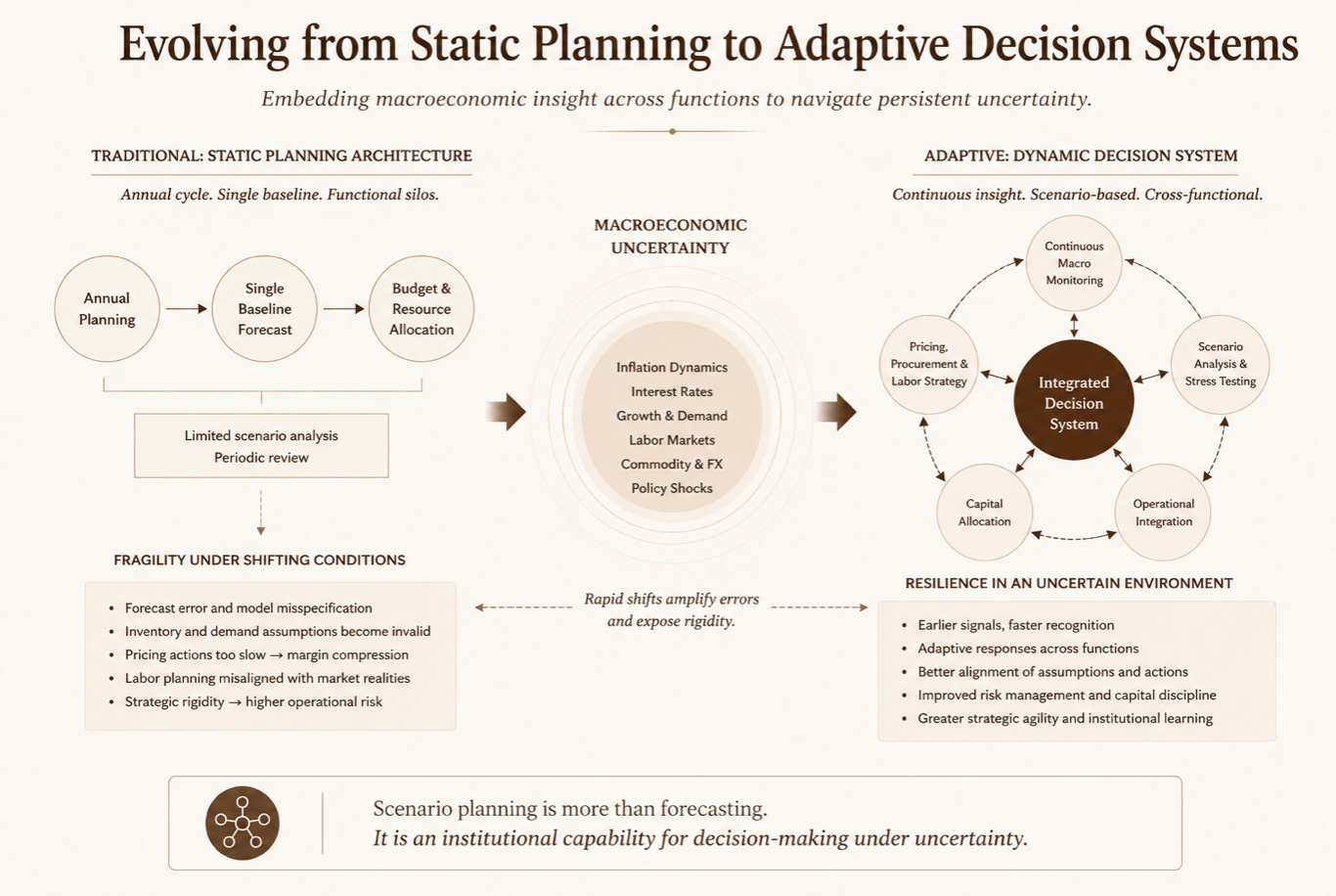

The Limits of Traditional Luxury Stratewgy Planning Architecture

Many luxury houses still plan on an annual cycle built around a single baseline, with limited testing of alternatives. The implicit assumption is continuity: that input costs hold, that trade conditions stay stable, and that any shortfall can be recovered through a further increase in price. That architecture was adequate while those assumptions held. It becomes fragile when they do not.

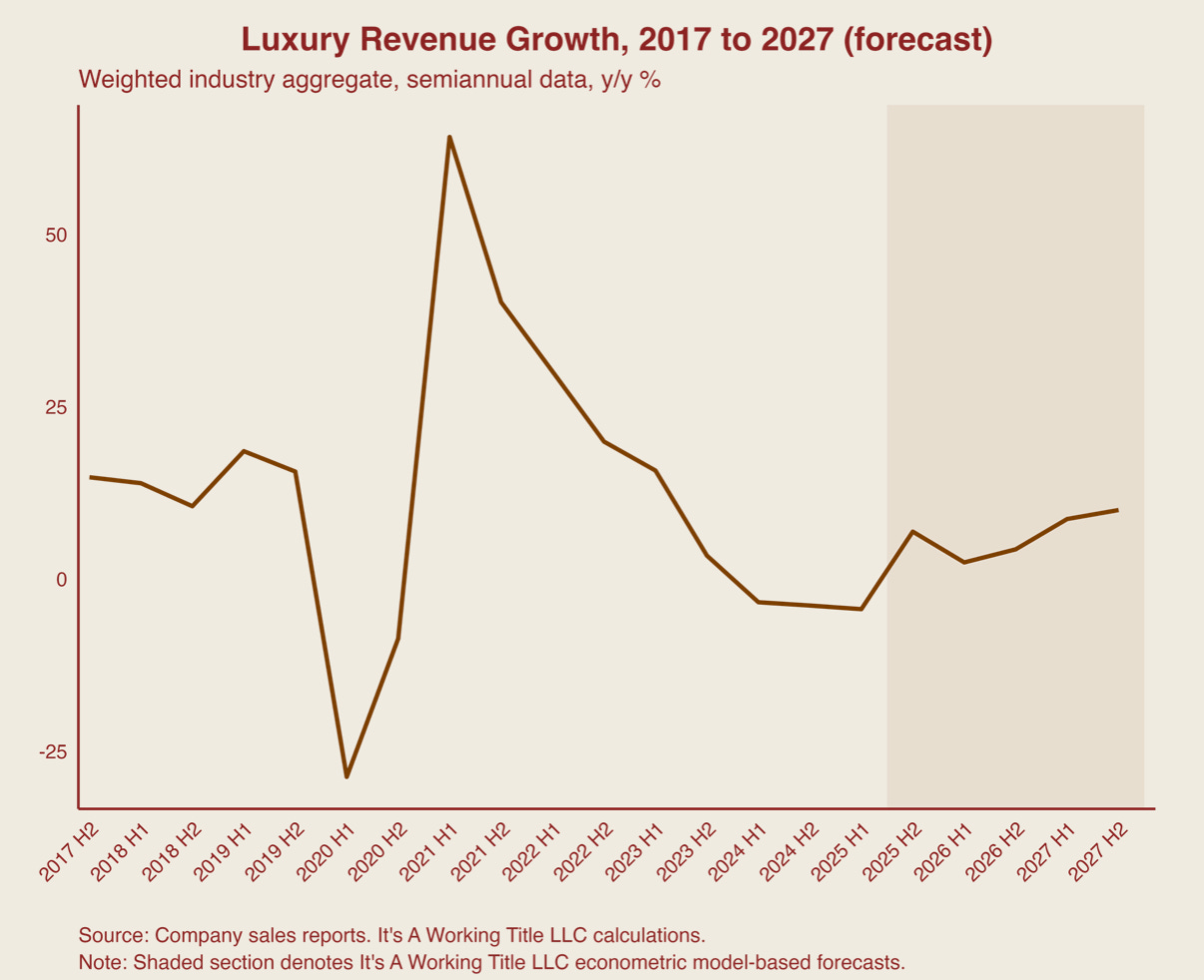

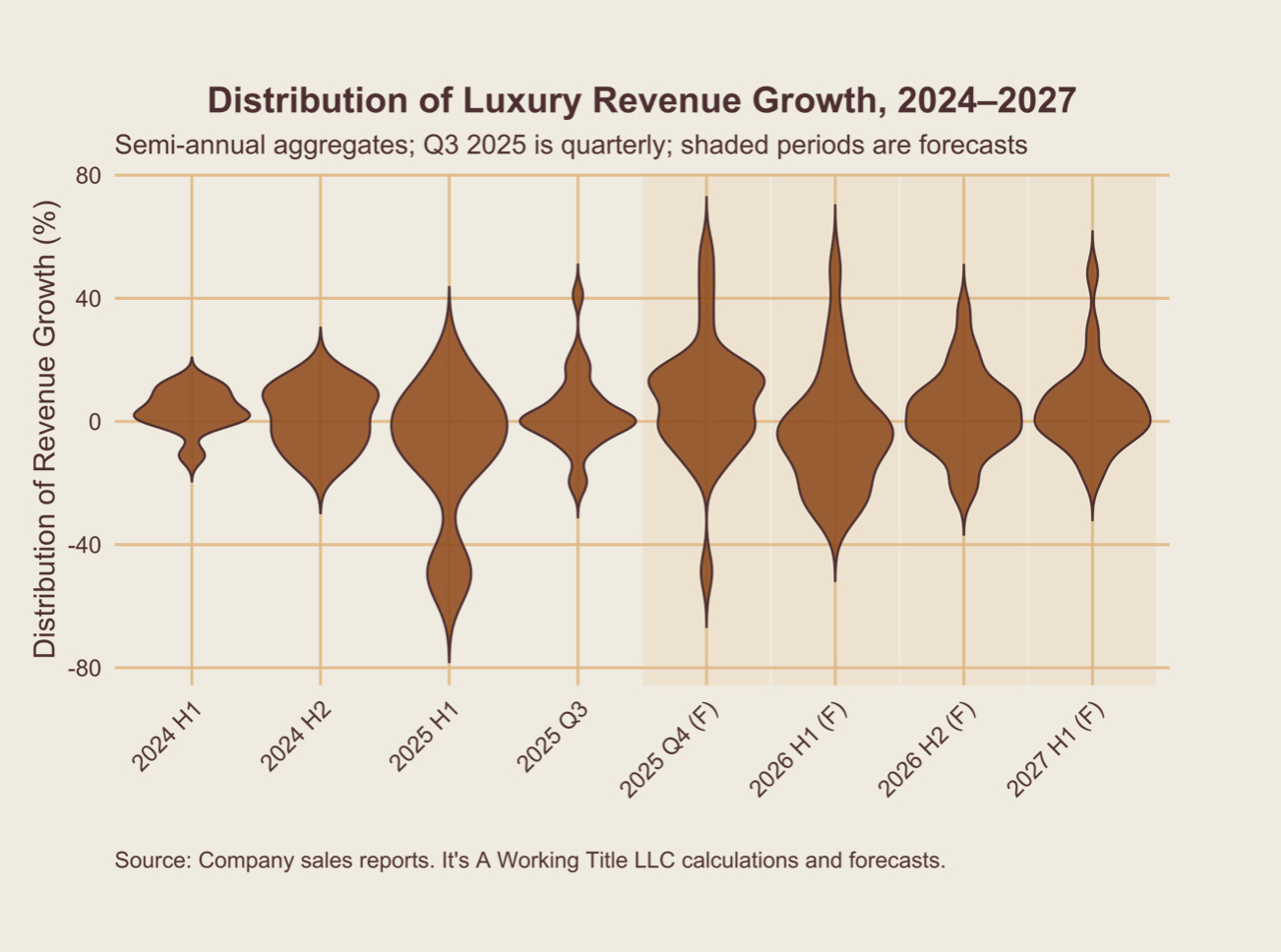

It is fragile in a second way. Planning to the industry average now means planning to a number that describes almost no one. IWT’s modeling shows the dispersion of luxury revenue growth widening from a standard deviation of eight to ten points before 2019 to above twenty, and into the forties, in recent periods; the full-year 2025 figure stood near twenty-two, easing only to the mid-teens by 2027 on our forecasts. A house that benchmarks to the average is calibrating to a market that no longer exists as one entity.

Experience has made the operational fragility concrete. A pricing cadence set once a year cannot track gold, which moves within weeks. A landed cost reset by a tariff cannot wait for the next round. And a price increase taken to protect margin can cost more in volume and brand perception than it recovers, because the elasticity the category long assumed away has reappeared. The houses responding best are embedding cost, currency and trade monitoring directly into pricing, sourcing and client decisions.

The shift is not only analytical; it is organizational, requiring coordination across creative, merchandising, pricing, supply chain, client relationships and finance. Yet the discipline needs care: a house that lets cost dictate the ticket erodes the desirability that justifies it. Discipline in the back office; conviction at the front.

Scenario Planning in an Era of Structural Uncertainty

The range of plausible outcomes facing luxury has widened across input costs, trade policy, the trajectory of Chinese demand and the confidence of clients.

In one path, cost pressure persists: gold stays elevated, tariffs settle in or expand, labor and materials costs hold. Hard luxury and leather goods face margin compression, pricing power is tested against a fatigued client, and demand redistributes toward lower-duty markets. The gap widens between scarcity-led houses, which can pass cost through, and volume players, which cannot.

In a second path, growth weakens while costs stay sticky. The aspirational base contracts, the top client plateaus, and duties hold. This is the most uncomfortable combination: a house can neither raise price without losing volume nor hold it without losing margin.

In a third path, cost pressure eases: gold corrects, tariffs revert toward their former base. Yet if relief comes through weaker conditions and a more cautious consumer, demand softens too, and the elevated price structures built in the high-cost period, especially in the United States, may have to be unwound.

The strategic challenge is not determining which path occurs. It is ensuring that leadership teams understand the operational implications of each before it does.

This is where scenario planning earns its place. Houses that have rehearsed how alternative conditions affect pricing, allocation, sourcing and demand respond more decisively, having already examined the moves. The signals are specific: gold and precious-material prices, the status of US tariffs, Swiss export data, Chinese confidence, the major currency pairs, and the secondary market, which often turns first.

Preparedness reduces reaction time. Where a misjudged price increase costs not only margin but desirability, the ability to adapt with conviction may matter more than any forecast.

Strategic Implications for Luxury Leadership Teams

Persistent inflation uncertainty is forcing luxury houses to reconsider assumptions that long sat beneath their planning. Pricing governance is becoming central to performance, as houses balance margin, desirability, retention and a newly visible elasticity at once. Sourcing and production are shaped by trade policy and resilience rather than cost alone, with manufacturing footprint and customs strategy now matters of strategy. Capital allocation is reweighed under higher financing costs. And client strategy has become a genuine choice, between defending the top tier and rebuilding the aspirational base the sector has lost.

Leadership teams are recognizing that speed and adaptability may matter more than optimization against a stable assumption. This does not mean abandoning the long view. Luxury, more than most industries, is built on continuity and the slow accumulation of authority. The framework around that long view must become more dynamic, without disturbing the consistency the brand requires.

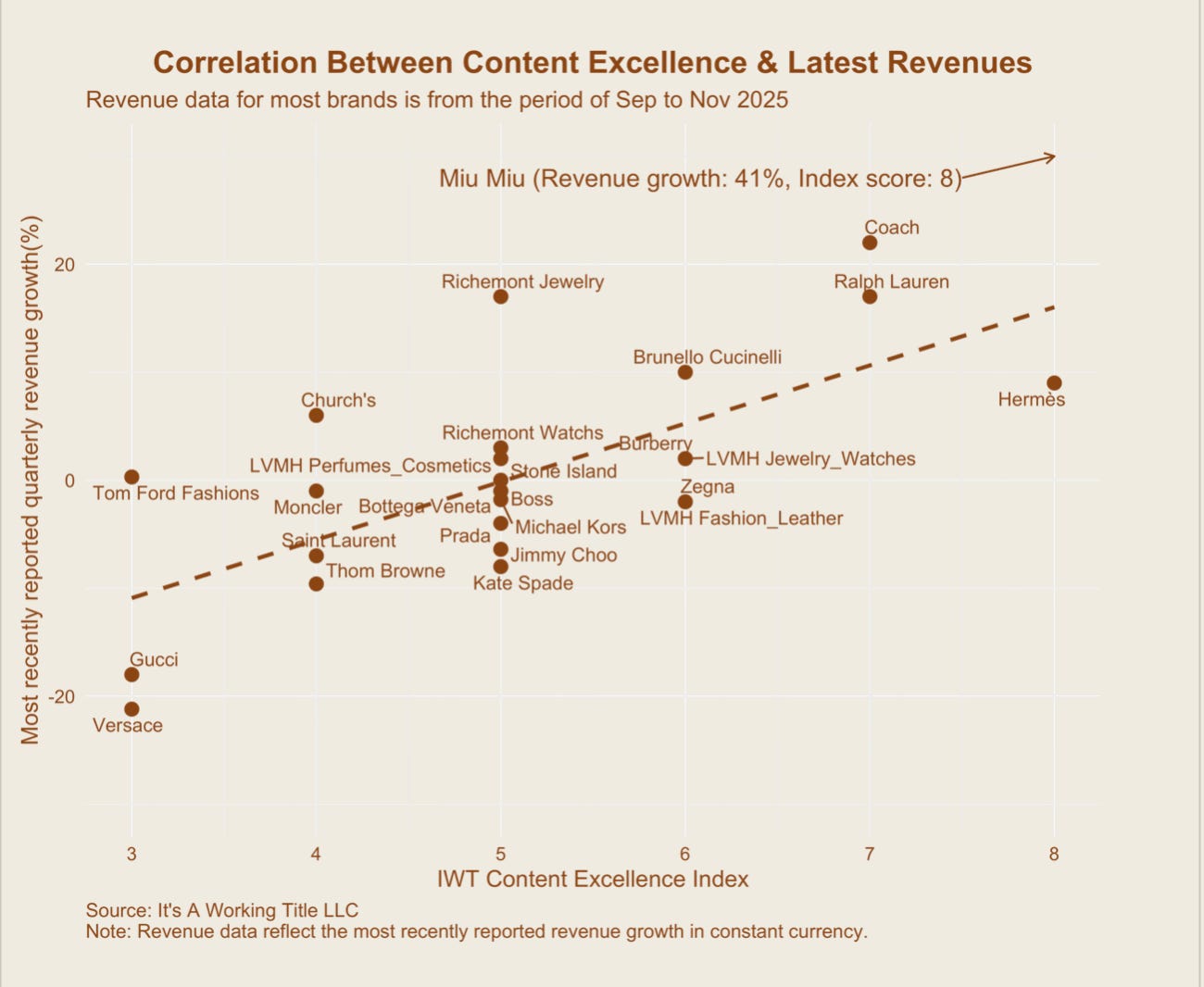

The evidence of the last two years points to one conclusion. The houses that grew through the downturn are not those that priced highest or spent loudest, but those operating from a coherent narrative system and disciplined architecture, the names atop the IWT Markets Content Effectiveness Index. Differentiation is not an outcome of the cycle; it is a built capability, the surest hedge against conditions a house cannot control.

Ultimately, the houses most likely to endure will not be those that forecast the cycle most precisely. They will be those that hold their brand authority steady while adapting the operating model around it. The art of desirability and the science of systems, held in tension, and resolved.