Building Luxury Brand Value Amid Geopolitical Economic Uncertainty

FSW examines the state of the luxury economy and how brands can use content strategy to build brand equity in a turbulent global market.

Insights

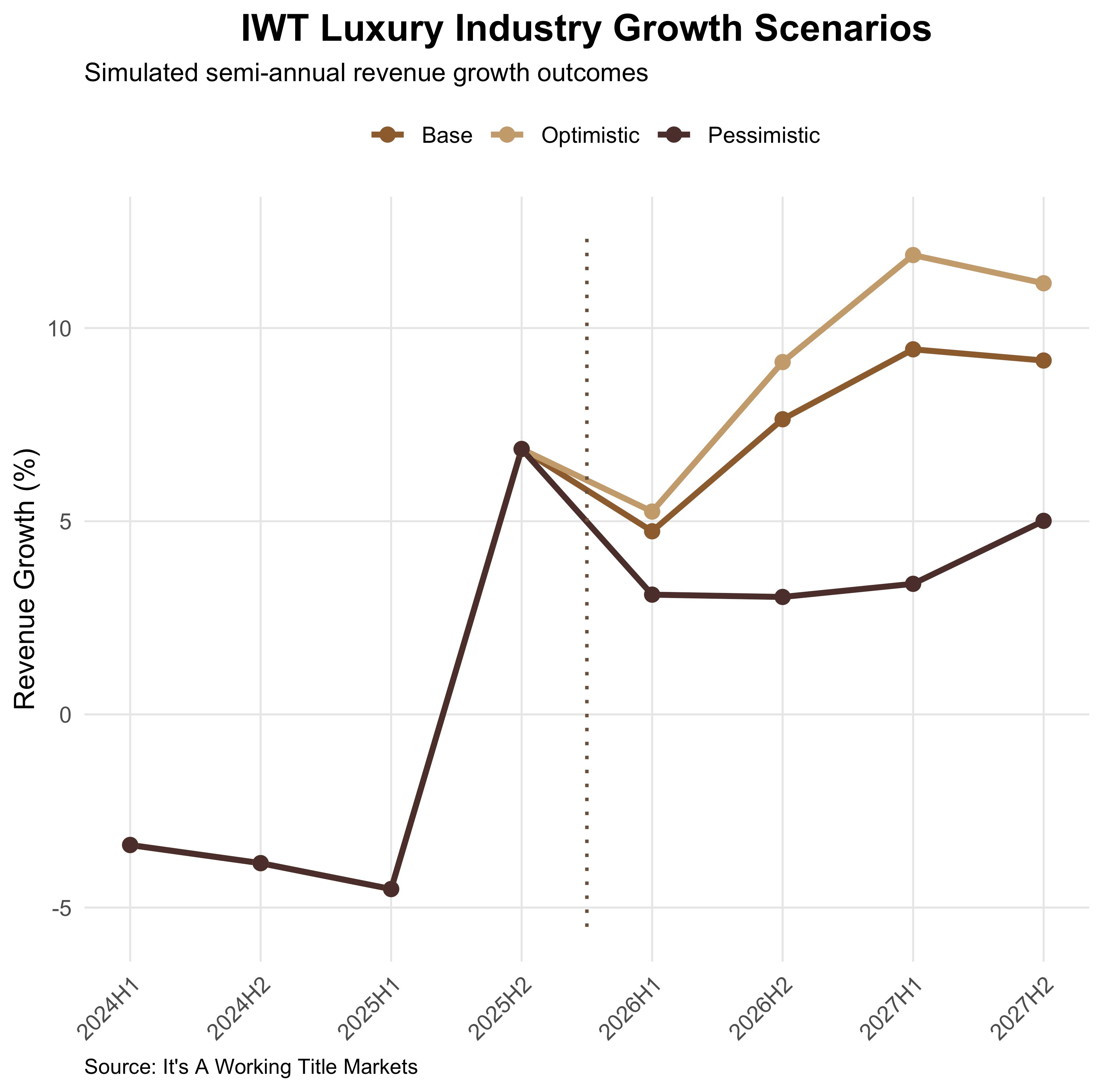

We present three simulations of luxury industry performance (base, optimistic, pessimistic) to capture how geopolitical risk and shifting macro conditions are widening the range of possible outcomes for discretionary demand, rather than pointing to a single recovery path.

While the sector has exited its downturn after a period of contraction driven by weak China demand and pricing pressures, the recovery is uneven and increasingly dependent on macro conditions, with growth returning across scenarios but varying meaningfully based on China, global growth, and financial conditions.

In this more volatile and dispersed environment, execution becomes a key differentiator, with brands needing stronger, more scalable content strategy and operations to localise effectively, engage consumers, and build resilience as demand becomes more fragmented and less predictable.

Geopolitical Economics is Driving Widely Diverging Prospects for Luxury

The waves of political and economic risk continue. Some of the near-term risks, such as slowing cyclical demand for premium and luxury goods in response to aggressive price hikes of the past few years, have been easy to forecast. Others, such as iterations of disruption to global trade policy and geopolitical developments, are more difficult.

By and large, luxury sales have held up rather well given the circumstances. After all, demand from the industry’s key growth market, China, remains moribund for many key brands. The industry even exited recession, by our count anyways, in Q4 2025 after six consecutive quarters of negative growth followed by the post-pandemic supercycle.

At the start of the year, we predicted modest, though positive, luxury industry growth this year and into 2027. (See “The Differentiation Economy: Why Narrative Systems Will Define Growth in the AI Era”.) Now, the range of possibilities seems quite a bit wider.

Three Simulations of Luxury Industry Performance in 2026-27

Geopolitical economic developments are driving a wider range of possible outcomes for discretionary spending than we’ve seen in recent years. For a sector so tightly linked to global wealth and sentiment, this matters disproportionately. Against that backdrop, we have used our proprietary sector-specific macro-econometric model to frame three distinct simulations—base, optimistic, and pessimistic—to understand how different macro paths translate into industry performance. For a sector so tightly linked to global wealth and sentiment, this matters disproportionately.

Each scenario is anchored in a coherent macro setup:

The base case assumes steady but unspectacular growth: China stabilising in the mid-4% range, the U.S. expanding around trend, energy prices remaining contained, and financial conditions broadly stable.

The optimistic case reflects a more supportive environment, with stronger Chinese growth, resilient U.S. demand, easing financial conditions, and lower energy prices reinforcing both confidence and spending.

The pessimistic case assumes a more challenging mix: weaker Chinese momentum, softer global growth, higher energy prices, and tighter financial conditions weighing on discretionary demand. Currency moves are incorporated as part of these broader conditions, acting as an additional source of variability in reported results.

The key takeaway is not the precise numbers, but the dispersion across outcomes. The sector has already moved through its downturn—2024 and early 2025 represent the trough—but what follows is not a synchronised rebound. Instead, growth resumes into a much wider range depending on the macro environment. In the base case, the industry settles into a steady mid-to-high single-digit growth trajectory. In the optimistic scenario, stronger macro conditions lift growth into low double digits. In the pessimistic case, growth compresses materially, but importantly, remains positive. That asymmetry is telling: luxury now appears to have a structural floor, but a more limited upside skew than in prior cycles.

China sits at the centre of this dynamic. Across all three simulations, it remains the most important marginal driver—but its role has evolved. The model assumes stabilisation rather than reacceleration, and that distinction matters. Even in a more favourable environment, stronger Chinese growth translates into improvement, not a return to the outsized expansion of the past decade. In a weaker environment, however, softer Chinese demand feeds through quickly into sector growth. The result is a more nonlinear sensitivity, where downside shocks have a larger impact than upside surprises.

The implication is that luxury is transitioning into a more balanced, but more macro-dependent regime. The U.S. provides a stabilising base of demand, China drives variability, and financial conditions—through equities, rates, and currencies—determine how much of that demand converts into growth. The three scenarios make this explicit: the industry is no longer operating in a one-way expansion cycle, but in a range of plausible macro environments with meaningfully different outcomes. For brands and investors alike, the message is clear: luxury remains structurally attractive, but understanding the macro context has become central to understanding the sector itself

Building Market Resilience through Applied Luxury Strategy

The resilience of luxury brands and their ability to flex and adapt for the future in shifting market dynamics should involve a combination of adaptability and long-term strategy. For luxury brands, this directly translates into how they plan, create, manage, and distribute content across and within channels.

The reality is that many luxury brands lack holistic content strategy and scalable content operations infrastructure, even if they have a strong digital and e-commerce foundation, complete with tools and platforms across the major retail tech acronyms, including PIM, DAM, CRM, and PCOS. Without content strategy, luxury brands suffer from many issues, including:

Lack of centralised content operations: Brand content teams are often siloed with too many disparate tools and disconnected, undocumented processes and guidelines. This makes executing consistent yet attenuated cross-channel campaigns hard to plan, create, personalise, and measure.

A reactive—even outdated—approach to content creation: Brands focus on immediate needs or short-term campaign tactics, instead of planning for volatility or original creative approaches.

Failure to scale globally with nuance: A lack of true regionalisation and localisation content strategy leads to content that may resonate with an American luxury buyer may miss the mark in other markets.

An underinvestment in data-driven storytelling: For all the attention brands give to data and analytics, many do not use consumer insights in a holistic, fully applied way to guide narrative design and content decision-making.

Why Luxury Content Strategy and Operations Matter in Uncertain Times

No brand needs blanket advice on strategy and staying ahead of trends in an uncertain global economy. Most brand strategists will tell you that what brands need is a core understanding of their own “why,” what the unique value add of their products are, who their target customers are, and how, where, when, and for what they shop. Yet, what brand strategy misses is the medium of exchange—the sharing of information and ideas—that inspires, informs, and drives customers to purchase. This is more than just marketing. It is the what, why, how, where, when, and why of content and how brands and their customers use and experience it.

Content comprises anywhere your target audiences encounter your brand messaging.

While getting content right is one among many factors that contribute to consumer purchase decisions, content is indelibly linked to brand storytelling for luxury brands and, in turn forms a key differentiating factor between luxury goods and services and other kinds of goods and services when it comes to customer value creation.

So what exactly can holistic content strategy and content operations do for luxury brands amid heighted geoeconomic uncertainty?

Here’s a handful of benefits:

1. Resilient Content Revenue Streams

With potential U.S. tariffs and shifting Chinese demand exacerbating economic volatility, content is how brands can build deeper relationships with consumers in existing markets while generating new ones.

Localised narratives can help brands identify and engage with new audiences in regions underrepresented in their sales mix without concerns over brand dilution.

Dynamic campaigns with the flexibility to scale or scale back with budget constraints can give brands flexibility during uncertain times. Basic processes like a documented creative brief intake form and workflow can help track new and ongoing projects.

2. Consumer-Centric Storytelling and Differentiation

For all the renewed attention on product-centric approaches to brand building and customer experience, luxury consumers are overwhelmed with content across channels as well as a multiplicity of ways to buy your products. To drive product discovery and purchase decisions, luxury brands need to guide consumers at every touchpoint of their shopping journey through appropriate and emotionally-engaging content.

Micro-storytelling through targeted campaigns and localised brand moments can draw in consumers through your brand’s unique value proposition and products.

Quality over quantity matters with luxury content to drive deeper engagement, product discovery, and brand loyalty, ideally in direct correlation with both customer retention and pricing strategies.

3. Operational Efficiency

Implementing a defined holistic content strategy astronomically reduces operational inefficiencies and internal spending by aligning marketing, branding, and creative teams under a single, integrated vision for brand content.

Where Brands Can Start with Luxury Content Strategy

Ultimately, luxury brands need content strategy now more than ever to hedge risks and differentiate themselves in an increasingly dispersed market environment. Yes, getting the product-pricing equation right matters to customer purchase decision-making. Yet, for high-net-worth and ultra-high-net-worth consumers, creating meaningful, truly elevated customer experiences through consistent, compelling, and channel-appropriate content and brand storytelling equally matters, particularly given the increasingly diffuse nature of most customer shopping journeys across touchpoints.

Some easy ways to start with holistic content strategy include:

Start with consumer and competitor research and targeting, using predictive modeling and consumer data to generate insights to allow your brand to anticipate market shifts and changing consumer content preferences and behaviours.

Focus on localisation and personalisation at scale, tailoring your content to align with cultural nuances of specific regions and locations.

Automate lower-level content functions like workflows and basic content production to integrate and streamline content operations across teams.

Create a holistic content strategy and operations model that meets your brand vision and consumer needs. This will help your brand create consistent and connected storytelling, diversified, dynamic content types, and integrated, effective content across and within channels.